Sortino Ratio: Definition, Formula, Calculation and Example

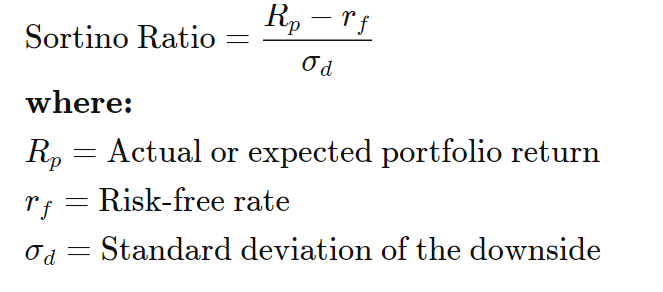

The Sortino Ratio is a variant of the Sharpe Ratio that separates harmful volatility from total overall volatility by using the asset’s standard deviation of negative portfolio returns – downward deviation – instead of the total standard deviation of portfolio returns. The Sortino ratio takes an asset or portfolio’s return and subtracts the risk-free rate, then divides that amount by the asset’s downside deviation. The relationship was named after Frank A. Sortino.

Formula and calculation of the Sortino ratio

The Sortino ratio differs from the Sharpe ratio in that it only takes into account the standard deviation of the downside risk, rather than that of the entire (upside + downside) risk.

Since the Sortino ratio focuses only on the negative deviation of a portfolio’s return from the mean, it is considered to provide a better picture of a portfolio’s risk-adjusted performance since positive volatility is a benefit.

The Sortino ratio is a useful way for investors, analysts and portfolio managers to evaluate an investment’s performance for a given level of bad risk.

The Sortino ratio is a useful way for investors, analysts and portfolio managers to evaluate an investment’s performance for a given level of bad risk. Because this ratio uses only the downside deviation as a risk measure, it solves the problem of using total risk, or standard deviation, which is important because upside volatility is beneficial to investors and is not a factor that most investors worry about.

Example of how to use the Sortino ratio

Like the Sharpe ratio, a higher Sortino ratio is better. When looking at two similar investments, a rational investor would prefer the one with the higher Sortino ratio because it means the investment earns more return per unit of the bad risk it takes.

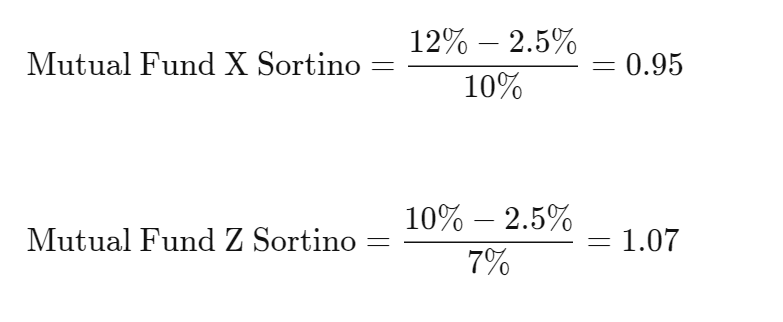

For example, suppose Fund X has an annual return of 12% and a downward deviation of 10%. Fund Z has an annual return of 10% and a downward deviation of 7%. The risk-free interest rate is 2.5%. The Sortino quotas for both funds would be calculated as:

Although Fund X returns 2% more on an annualized basis, it does not earn that return as efficiently as Fund Z, given their downward bias. Based on this measure, Fund Z is the better investment choice.

Although Fund X returns 2% more on an annualized basis, it does not earn that return as efficiently as Fund Z, given their downward bias. Based on this measure, Fund Z is the better investment choice.

While it is common to use the risk-free rate of return, investors can also use expected returns in calculations. To keep the formulas accurate, the investor should be consistent in terms of the type of return.

The difference between the Sortino ratio and the Sharpe ratio

The Sortino ratio improves the Sharpe ratio by isolating downside or negative volatility from total volatility by dividing the excess return by the downside deviation instead of the total standard deviation of a portfolio or asset.

The Sharpe ratio penalizes the investment for good risk, resulting in positive returns for investors. But deciding which ratio to use depends on whether the investor wants to focus on total or standard deviation, or just downward deviation.

About the Viking

With Viking’s signals, you have a good chance of finding the winners and selling in time. There are many securities. With Viking’s autopilots or tables, you can sort out the most interesting ETFs, stocks, options, warrants, funds, and so on. Vikingen is one of Sweden’s oldest equity research programs.

Click here to see what Vikingen offers: Detailed comparison – Stock market program for those who want to get even richer (vikingen.se)